Index based investment using a company’s total stock market value is a great concept and indexes such as the S&P 500 generally provide solid low cost diversification.

Unfortunately, Wall Street has now applied this concept to “sectors” of the stock market without adjusting for the size of individual companies. This is not only exposing investors to added risk due to poor diversification yet also handicapping newer smaller companies on which the future economy is dependent.

Let’s take a look at the two largest holdings in the MSCI Health Care Sector Index. An index used by more than 97 percent of all large fund managers.

The problem is simply that the MSCI sector funds, like the health care fund, are weighted based upon market cap, a company’s total stock market value, with no practical limits on individual companies.

What this means is that Johnson and Johnson, while 1.7 percent of the S&P 500 stock index, becomes 10.5 percent of the MSCI Healthcare Index. The second largest holding, Pfizer, represents approximately 1 percent of the S&P 500 yet 5.6 percent of the healthcare index.

Here is an overall snapshot of the MSCI Health Care index followed by two leading health care funds using the index. This MSCI health care index is composed of companies with a market cap of approx 3.5 trillion, roughly 16 percent of the S&P 500 market cap of 21.5 trillion. Note that 44 percent of the entire index is just 10 companies.

All the big fund families, including Vanguard and State Street, seem to be indexing to the same health care index, the MSCI. Other MSCI funds are equally popular, including the 10 following Vanguard funds based exclusively on other MSCI sector indexes.

One might ask, who owns MSCI given its enormous clout regarding where investment dollars flow in addition to its being used for performance benchmarks?

One might ask, who owns MSCI given its enormous clout regarding where investment dollars flow in addition to its being used for performance benchmarks?

MSCI (formerly Morgan Stanley Capital International) is a publicly traded company, ticker MSCI, in which Vanguard, Fidelity and BlackRock collectively own 30 percent of all shares outstanding.

MSCI indexes are used by 97 percent of all large investment funds, both in allocating capital and establishing performance benchmarks.

MSCI’s 3 largest shareholders:

Remarkably non of these major MSCI shareholders seem concerned about the fundamental flaw in using MSCI’s sector indexes given that they are all generally based exclusively on each firms market capitalization as a percent of the S&P 500. Clearly a great opportunity exists for a competitor to MSCI to emerge using better diversified indexes.

Vanguard, Fidelity and BlackRock seem to have forgotten that the key benefit to index based investment is indeed diversification. For example, 44 percent of the Vanguard Healthcare assets in its ETF fund, and all other similar funds using this index, are represented by just 10 companies, with Johnson and Johnson alone representing more than 10 and Pfizer 5 percent of the total index.

In addition, major institutional investors like public pensions, foundations and endowments are also relying on the same MSCI Health care index when it comes to health care investments and related performance evaluations.

Of course this creates intense pressure for Johnson and Johnson, Pfizer and other major top 10 holdings to meet earnings and sales goals. Many could argue that this pressure is a factor in them billing the government excessive drug costs via medicare and medicaid in an attempt to sustain stock prices driven by the MSCI index, rather than company fundamentals.

One such technique is the major drug companies making contributions to tax exempt foundations that in turn will help patients afford expensive drugs. See Regeneron Post below for mechanics on how this scheme works.

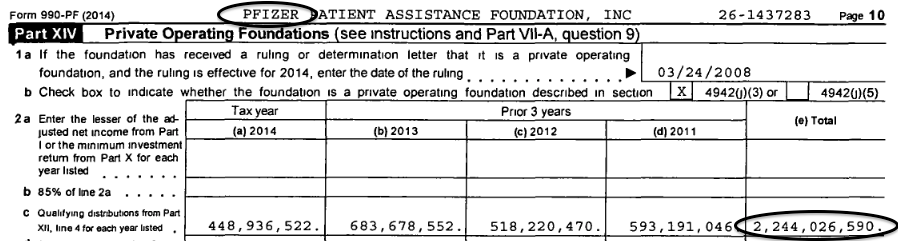

The net impact is to sustain artificially high drug prices, i.e. manipulate earnings. Pfizer alone contributed approx $2.2 billion to one such foundation from 2011-2014. See below from Pfizer Foundation’s 2014 filing:

One could also argue that these practices have created a pyramid like scheme in which patients needing health care, and employees needing cost effective health insurance plans in order to inspire risk taking to form new businesses and stimulate the economy, are short changed.

Indeed, in 2017 Pfizer rolled out a new stock option program for employees, a circa 1999 like earnings management strategy, to reduce compensation expense. The reported costs on options, although compensation, won’t impact earnings as much as compensation paid in cash. Much better for both employees and investors are restricted stock programs that vest 20 percent per year.

This is perhaps the big related untold story behind the mortgage meltdown in 2008 in which private equity and hedge funds “flipped” mortgages in order to inflate income on which stock option based carried interest was paid.

See related posts on royalty pharma and Regeneron on how private equity firms are issuing bonds that securitize future drug payments on Johnson and Johnson, Pfizer and other major drug-makers drugs, using patient health as collateral. The parallel to the mortgage situation is explained in the blog post below.

Patient Health: https://blog.billparish.com/2017/07/19/is-patient-health-being-mortgaged-via-derivatives-as-homes-were-during-the-financial-crisis/

Drug Costs: https://blog.billparish.com/2017/07/25/regenerons-eylea-pulling-open-the-curtain-on-drug-costs/

Many of these large drug companies driving the MSCI index, unlike leading technology companies in the 1990’s, now also have significant long term debt and related interest charges that will contain future earnings growth. For this reason, they invest less in R&D and are instead purchasing the rights to various medications and spending more resources on packaging and marketing.

The key point here is that using the MSCI Health Care Index that relies only on market capitalization of S&P 500 listed companies is not only by nature dysfunctional yet also lazy.

With the current CEO of MSCI, Henry Fernandez, owning more than $100 million in MSCI stock, perhaps it’s also a good time for Henry to sharpen his pencil , examine the quality of the indexes and innovate. Many investment advisors like myself would be delighted to have exposure to higher quality choices in the health care space.

MSCI CEO, Henry Fernandez