While the media is sensationalizing Intel CEO Brian Krzanich’s recent stock sales as unusual given the recently disclosed security weakness in Intel’s chips, a closer look reveals excellent tax planning, to the benefit of the company.

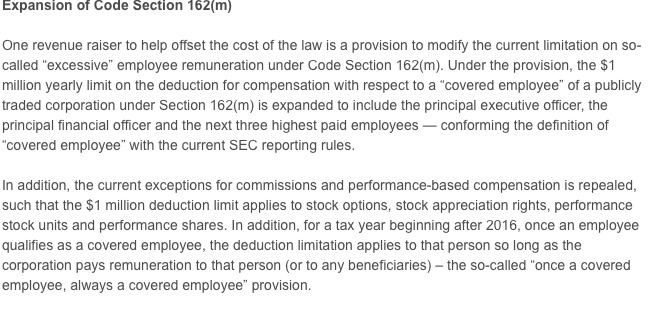

One of the key changes in the new tax law, a good one, is to expand the definition of compensation subject to the annual $1 million limit with respect to receiving a tax deduction. Previously, only cash compensation was subject to the limit yet now all equity based compensation is also included, including stock options.

What this means is that if Intel’s CEO, for example, would have waited until after January 1st to exercise $25 million in options, the company would receive no tax deduction yet exercising prior to January 1 provides Intel a $25 million tax deduction.

Remarkably, not even the Wall Street Journal has reported this key fact. Throughout the month of December, whenever called by reporters, I asked why no one was convering this new rule. The obvious reason being that after December 31st the deductions are lost.

See key WSJ story excerpt below followed by summary of new legal change from independent tax related website. This is an excellent story yet like many such stories they are too focused upon supporting the reporters “angle” and not respective of all supporting facts.

Yes, the new law was not technically approved by the Senate until December 2nd and the sales were November 29th yet clearly this change was one that was coming. So rather than make hay for class action attorneys looking to milk shareholders for contingent fees in return for a few pennies a share settlement for shareholders, how about recognizing how beneficial this was to the company.

Sadly, the business media refused to do a high profile story in December that might have encouraged many other top execs to do the same, greatly benefiting their respective companies. Especially in those cases where the sales would have occurred with 18 months anyway.

Summary Description of New Executive Compensation Rules